With so many focused on calling the bottom it would be easy to get so caught up in price action that you miss the bigger picture. The “institutions are buying” meme has become so trite as to risk being ignored completely -particularly after the everything selloff that has occurred in almost every risk-on asset imaginable. The only problem with that is institutions ARE buying and, as a long term investor, these are the things we need to be keeping our eyes on.

Silvergate Bank (NYSE:SI) was long touted as, aside from Coinbase, the true picks-and-shovels investment in crypto. As an early mover in providing traditional banking services to crypto exchanges it benefited from an unparalleled level of market penetration. In Q4 of 2021, the Silvergate Exchange Network (SEN) processed a mindboggling $219.2B in transfers across its clients, up 35% from the prior quarter and an increase of 270% from Q4 2020. While agnostic to crypto prices to some degree it was not altogether insulated from the nukes of 2022 and suffered quarter after quarter declines, with a total of $563.3B processed through SEN down from $787.4B a year earlier (a 28.5% drop). The stock price followed recording a 95.5% drop from its high in November 2021. At the start of January there began rumours of a bank run following the collapse of FTX, and solvency issues surrounding Grayscale and DCG. These rumours proved to be unfounded. On January 31, 2022 an SEC filing showed BlackRock had increased it’s stake in Silvergate to 7.2% from 5.9% a year earlier. On February 2, State Street disclosed in an SEC filing that it has taken a 9.32% stake in the bank. Fast forward to today, both Citadel Securities and Susquehanna Advisors disclose they bought 5.5% and 7.5% interest in the beleaguered bank, respectively.

But what business does Citadel in Susquehanna have with an interest in Silvergate? Well, Citadel was more recently known for its stake in Robinhood and controversy erupted around its Market Maker role on the app. It is largely known that in exchange for no-fee trading Citadel not only provides order routing on Robinhood’s platform but has complete view of all of the trades. Citadel itself accounts for over 10% of US equity trading volume. Susquehanna is largely known for its expertise in high frequency trading and similarly holds a top spot in total US flows, handling over 7% of all ETF volume back in 2018. When the execution arms of three of the largest asset managers in the world buy a stake that triggers a 13D Schedule notice you have to take note. Add all the interests up you get almost 30%. That’s already past the minority threshold, but maybe there were similar entities with stakes lower than 5%? Add those up and maybe you get more than 50%? One thing is certain, you have some of the largest volume traders on US securities seeing considerable value in an intermediary that handled the majority of cash moving between crypto and the regulated US financial system.

I’m borrowing from Barry Ritholtz – The Big Picture’s link list format as there’s little else to talk about while nature heals itself (after the recent crypto credit implosion / nuclear winter). Some really good articles I need to recommend while we all watch our Ledger NAV’s come back:

Great article in the Atlantic came out on right before the holidays, by Adam Kirsch. A good friend of mine is actually a Doomer and I consider there to be several subsets of Doomers, but his is the classic one what Adam refers to as an Anthropocene anti-humanist. While I don’t believe he is really anti-humanist, more-so he is opposed to society’s relentless consumption of natural resources and is really just pro-earth, but has volunteered with XR and is aligned with most of that organization’s viewpoints. His thesis, in comparison, is better represented by the book Less is More by Jason Hickel and is essentially an essay to further an argument advocating central planning and rationing. I won’t get into detail on how it’s totally infeasible and ignores humanity’s selfish natures (and ultimately international realpolitik), because then I would just be regurgitating my Jurisprudence course material with heavy references to Thomas Hobbes, and run the risk of slipping into a geopolitical ramble. Instead, it’s more interesting to focus on the ideas and concepts discussed in the article. I must confess I myself am a transhumanist and can’t wait to evolve out of my limited fleshy form. Imagine sharing the processing power of a supercomputer and adopting an exoskeleton to augment your physical abilities. My only disappointment is that we aren’t already cyborgs, but I digress. It really comes down to what we as humans are all about. Are we going to put technological advancement on pause and work out how best to allocate what finite resources are left among the population? Or are we going to continue to push forward and embrace change, potentially destroying things along the way but hopefully inventing new solutions that expand the pie rather than divvy out the pieces? My money, and my philosophies, lie with the latter. I firmly believe that this new anti-humanist (and really anti-progress) movement is simply a modern day version of the counterculture of the 1960’s, and I can’t wait for it to be over. Anyway, the article is fantastic and balanced, and I encourage everyone to explore the ideas it touches upon.

Arthur’s Hayes’ latest article Vitiligo is yet another macro-opinion piece written in the Michael Lewis style. Reading Arthur’s articles you can tell he is not shy about owing his inspiration to Lewis, and I think it very much compliments the subject matter. In fact when you look at both Arthur and Lewis -both had stints at big banks, both maintain the appropriate balance of objectivity and use of sarcasm (for effect), and both are very clever writers. I did find Arthur’s commentary on the east and west geopolitical dynamic interesting and relevant, and I confess many of his opinions mirror my own, particularly around international finance and organizational dynamics. It reaffirms my own view regarding the west’s role in the fight on climate change -that it completely ignores the realpolitik and the geopolitical moves of our aggressors. As a side note, our enemies do not care about climate, rather they want to promise better lives for their citizenry and outcompete us in trade and production. Moreover, it is our government’s responsibility to help secure cheap inputs and keep inflation low, not raise taxes on our consumption. Doing so unravels the progress made by globalization and increases the time it takes for us to progress to the next technological era. If only environmentalists would realize fossil fuels are simply a stepping stone to be used in advancing clean energy sources, not the be-all and end-all.

I’ll end this post with a bit of a link soup. On The Brink hosted Tom Emmer for a podcast that really restored my confidence in some members of Congress. What surprises me is the number of people I know sending messages to the effect of “I told you so” or “crypto is a scam” as if FTX/FTT comprised the majority of crypto’s market cap. What I love about Tom is his ability to communicate the rebuttal to this so effectively as a politician. Since the popular press is wholly owned by TradFi it’s not a surprise we aren’t receiving any journalistic help from them. Also nice to see politicians place the blame where it should be, on the regulator, just like in 2008. Second up is Framework doing a fantastic episode on Bell Curve going over FTX, L1s, crypto macro, and even ChatGPT. I just love hearing this VC present their thoughts. And the discussion of a time where an invention came out that completely changed how you thought about something is just so inspiring. I really encourage everyone to watch the full episode.

A great article from The Atlantic came out last Friday. There was some good discussion of how the Internet challenged the business model for advertising and leveled the playing field for authorship (of which this article is yet another example). And while it did highlight the role that primarily NFTs will have on the further digitalization of our economy, financial or otherwise, it fell short of explaining why that was even a good thing at all. This post aims to provide a possible explanation as to why crypto, NFTs, Decentralized Finance (DeFi), and Web 3.0 as a whole, are the next logical step in the evolution of our (arguably credit based) economy.

As Niall Furgeson writes in The Ascent of Money, “Credit and debt, in short, are among the essential building blocks of economic development, as vital to creating the wealth of nations as mining, manufacturing or mobile telephony”. The emergence of banking with the invention of double entry bookkeeping and the system of debits and credits set the stage for unprecedented economic growth. While the industrial revolution introduced technological improvements it was through statement of accounts and the transacting of assets along with liabilities that made commerce recordable, profitable, and thus possible. The establishment of the central bank as the “lender of last resort” was the final step in guaranteeing the debts of a long chain of producers and consumers. People are willing to transact largely because an intermediary is able to guarantee the debts of an individual or business. If a ship is carrying oil across the Atlantic it does so because there is a Bill of Lading that is transferable and accepted by a purchasing party, and the party selling the oil is satisfied as to the creditworthiness of the purchaser. Commerce is made possible by the use of legal documents enforceable in a court of law, and intermediaries acting as guarantors on the debts of the transacting parties.

Without the expansion of credit economic growth would not, and still to this day cannot, be possible. It is through the promise of profit that employees are willing to sacrifice their time, or the purchasers of a business are willing to surrender their capital, for the purposes of a venture. For someone to get out of bed in the morning they must be convinced they will have more tomorrow than they have today, ie. the promise of a return. The famous Supreme Court case SEC v. W. J. Howey Co is used in the United States, for example, to determine whether there exists an “investment contract” for the purposes of the Securities Act, or rather: “a contract, transaction or scheme whereby a person invests his money in a common enterprise and is led to expect profits solely from the efforts of the promoter or a third party.” Bonds charge a percent interest coupon in exchange for the principal amount borrowed. The central bank sets interest rates that commercial banks use to set their market rates for lending. The profitability of companies is largely dependent on market rates for lending as it is the driver for how much inventory a company can hold. Those that borrow too much and sell too little go bankrupt. Companies that sit on too much cash and fail to grow the business are punished by shareholders. Similar to corporate executives, governments officials are elected to ensure the economy keeps expanding at a steady rate (among other things, although job growth is a chief concern). The government has a responsibility to expand the economy and spends money to stimulate growth, and the central bank supports them by keeping interest rates just low enough as to avoid bringing about inflation.

This dynamic becomes a positive feedback loop as capital is reinvested for the purpose of creating profit, workers are paid more and thus increase their consumption, and everyone (including the government) borrows more money to keep this going. This is the expansion of credit and it underpins all of our accelerated growth over the past couple hundred years. Time and time again, in the face of a looming recession the government has stepped in to stimulate the economy through public spending, and the central bank has opted for expansionary monetary policy by lowering interest rates. More recently, central banks have made direct purchases of both government and corporate debt to put downward pressure on interest rates. This works until it doesn’t as central banks are eventually challenged by both inflation and other IS-LM dangers of a zero interest rate policy (ZIRP) trap. This is what Japan faced in its lost decade spanning the 1990’s. Brought on by interest rate hikes in response to an overheating real estate market the problem faced by the Bank of Japan was twofold: economic stagnation coupled with a decline in asset prices, made worse by a credit crisis stemming from lower rates (poor on fixed income) and the deleveraging. Central banks today are caught between the pressure to lower rates and stoke more growth, or raise rates to cool (serious) inflation concerns.

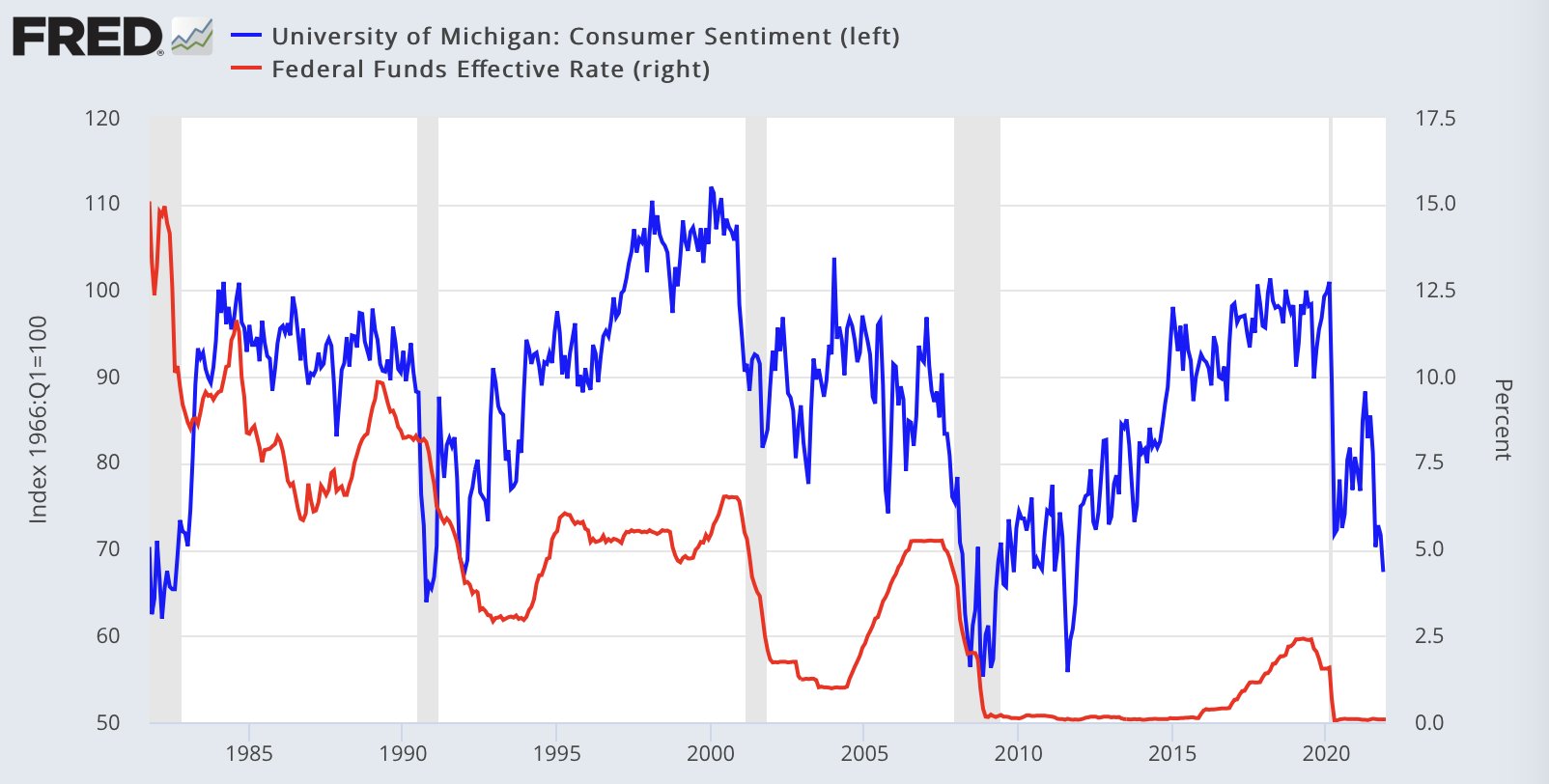

Rate hikes have been followed by a collapse in consumer sentiment

The tricky part lately is that it is questionable that the US economy can survive 6-7 rate hikes without kicking off a similar deleveraging as Japan during its “Lost Decade”. It is safe to assume that central banks are now limited in their ability to stoke economic growth through monetary policy. The start of 2022 saw a huge negative response to a hawkish Fed with the S&P correcting 12.35% from the high and the Nasdaq plummeting close to 20%! What is also worrisome is the response to the 10-2 year yield spread:

Yield quickly flattening in response to Fed announcements

Historically, the 10-2 spread has been a leading indicator of US recessions. With the yield curve for US Treasuries flattening there is a disincentive for investors to lend further out. This distorts credit markets and creates additional deflationary concerns. A slowdown in the US (and global) economy would be disastrous given how overstretched P/Es have become relative to the S&P 500. Here is the consensus on rate hikes for the year according to the major banks:

Fortune Magazine

With both the S&P and Nasdaq retracing their January dumps it is reasonable to assume the market has priced in these rate hikes. With the Fed effectively out of moves and the US government unable to pass any meaningful stimulus bills the question is: where will additional credit expansion come from?

Out of all potential benefits crypto has to offer (through disruption) the most meaningful to economic growth will be the boost to credit creation. Regardless, it is poised to touch on several key areas:

DeFi and smart contracts replace the intermediaries required to facilitate transactions.

NFTs and DeFi allow users to digitalize real-world things into data that can be further monetized (and collateralized).

Web 3.0 and DeFi allows individuals to act as their own lenders.

The benefit of making everyone their own investment banker is that we can allow people to incorporate more things into their net worth through digitalization. Having a record of ownership of not just data but of items not previously associated a dollar value (to be determined by online marketplaces) introduces a whole new dimension of credit previously left unrecognized. Smart contracts also help lower transaction costs via automation eliminating the friction inherent in intermediaries. Lawyers and accountants are expensive, and in an on-chain world, effectively redundant. While some degree of human intervention will be required, most standardized transactions involving property and trusts (for example) can be completely automated. The most frequently referenced chart in the DeFi space is the Total Value Locked (TVL) which represents the total US dollar value of crypto locked in DeFi smart contracts:

Despite the November-January crash this is holding up well

TOTAL market cap of the crypto universe

With increasing regulatory accommodation of stablecoins it is becoming increasingly difficult to ignore crypto’s contribution to overall credit expansion. It is only a matter of time until professional economists officially include crypto’s total market cap in the global M3+ numbers. Due to their liquid nature (cryptos can be very easily converted to cash) the total money supply MUST include these numbers. This is important because it increases the supply of credit circulating in the (now global) economy, and credit growth can now happen independent of the central bank. Because the Fed is unable to continue expanding credit due to inflationary concerns (and thus the money supply) we must look to new avenues or face asset deflation that brings about subsequent deleveraging (and further asset deflation).

Tides are the rise and fall of huge amounts of water due to the gravitational forces playing out between Earth and the surrounding celestial bodies, as well as the interactions between tectonic plates. Waves, which may be confused with tides, are disturbances in water that form solely due to the effect of powerful winds. Generally speaking, the tide moving in and out of a bay or shoreline is driven from forces far more powerful than those ebbs and flows licking up water for surfers to play in. This differentiation is particularly true for markets.

El Salvador’s President announced the debut of a bitcoin-linked bond offering on November 20th that caught many by surprise. The details released were as follows:

$1B face value, 6.5% coupon

Half to be spent on bitcoin purchases, half on infrastructure

10-year duration, matures 2032

Bitfinex is the bookrunner

Funding currencies are USD, USDT, and BTC

Backed by the government of El Salvador

No formal credit rating

Furthermore, 50% of the BTC purchased will be returned to investors once the initial $500m BTC investment has recovered. This additional “interest” is to be payable annually in January and the lockup on the BTC is 5 years. Questions remain around what the staggered payment schedule looks like after year 5 and how the deposits by/to investors will be handled by iFinex, as presumably the security will be listed and traded via the Bitfinex platform. Of the $500m directed toward “infrastructure” El Salvador claims it will be spent on the “bitcoin volcano”, a geothermal project designed to run a BTC mine linked via satellite through Blockstream.

There. That was convoluted -let’s untangle this. The $500m infrastructure investment appears to be your run of the mill sovereign debt issuance, although given El Salvador’s doghouse reputation with the IMF their current credit rating is high-risk with their 10-year currently trading at a 13% yield (junk). So if we were to value this bond at the same yield that face value drops on day one of trading. Thus the added feature of the BTC dividends after year five, or the “kicker” in common finance parlance, which serves to make this hybrid security (understatement) closer to a step up bond. In theory, after year five and assuming BTC is sold above the weighted average purchase price for a total amount value in excess of $500m, the investor collects not just the 6.5% coupon but an additional dividend from those excess returns depending on the spread. This was presumably done because in order to make this desirable for El Salvador they wanted to be below market on the coupon but give investors the right to some upside on BTC to keep them in line with market. In our view, if you’re a bull you’re probably better off just longing BTC directly through other means (spot, futures, perps, etc).

Now let’s take a look at the announcement made by Société Générale-Forge on September 30th where they plan to tokenize an existing covered bond they issued in May of 2020. Without getting into the specific mechanics of the on-chain, basically what they are proposing to do is take an existing security they tokenized on Ethereum and use it as collateral to mint DAI on Maker. Let’s look at the details:

EUR 40m face value, 0% coupon

5-year duration, matures 2025

SG is the underwriter

Funding currencies are EUR (CBDC), OFH tokens and ETH

Backed by residential mortgages and French/EU law

Rated aaa by Moody’s and AAA by Fitch

Now this experimentation started with SG back in April of 2019 when they first issued a EUR 100m of covered bonds on Ethereum that were subsequently made into OFH tokens. From a trading point of view there’s little to talk about here as the bonds offer a whopping 0% coupon.

From a technology perspective, however, the implications of this succeeding are staggering and amount to nothing less than a historic achievement. The ability to issue AAA rated bonds on-chain and collateralize them to mint stables will be known as an inflection point in modern finance. This is the holy grail. Anyone in finance with even a fleeting memory of the 1980s knows the impact the bond market had on Wall Street. The market for traded securities exploded throughout the 70’s and 80’s largely due to the ability for companies and people to freely trade in various grades of debt and equity. However, none of this would be possible without the establishment of central clearinghouses to standardize and create a marketplace for these securities. I’ve personally been bullish on Maker for a long time, specifically proposals to mint DAI backed by US treasuries as a means to bootstrap the money supply, but have since closed out my position due to a lack of performance relative to peers. We at TruBlock still believe a key driver to future DeFi growth is not just user adoption but putting high grade debt on-chain for use as collateral for digital assets.

Securities Industry and Financial Markets Association (SIFMA)

This isn’t a dig at El Salvador or what it has managed to achieve. It is hard to criticize their desire to gain independence from the IMF’s monetary and fiscal control. Seeing those Bitcoin bonds successfully traded on Bitfinex helps the crypto case, for sure. However, the success of fringe countries to raise debt outside of the global monetary system pales in consequence to the onboarding of the world’s financial system onto the blockchain. Just imagine if 50% of the $27T fixed income market was on-chain and collateralizing $6.75T (50% C-Ratio) in stablecoin equivalents. That is the TAM. That is the size of the prize. That is gravity raising the ocean level to lift all boats. That is the tide versus the wave.

Taken from The Block Crypto Dashboard (November 1, 2021)

A difficult to ignore knock-on effect of the ProShares Bitcoin Strategy ETF (BITO) has been the associated step-change increase in CME futures open interest. As with every other futures-based ETF pricing and settlement is made on the CME traded BTC futures contract, XBT. This requires additional XBT contracts to be opened as more money is invested into the ETF. Furthermore, as these contracts reach their delivery date the contracts must be closed and new XBT contracts are opened (this is known as a “roll”). As a reminder to the reader, these are cash-settled futures contracts and no transfer or ownership of the underlying is required. Why the regulator approved this instead of a spot ETF is perplexing, given the CFTC and SEC’s past criticism of various crypto exchange’s handling of non-physical settlement. While this jump in OI was expected the result has been a considerable shift in liquidity concentration across the major exchanges:

Total BTC Futures Open Interest by Exchange

Added competition from FTX and Bybit has helped boost aggregate OI to a whopping $24.4B as of November 1st. Crypto crackdowns in China has all but decimated the Asian exchanges. While Binance has always been able to keep the top spot the CME has been lagging prior to BITO’s approval. With almost 19% of total OI, one must assume that the SEC’s intended goal here was to give US-regulated exchanges greater impact on BTC’s overall pricing. The question left for traders is what impact increased participation by institutions will have over long-term volatility. Now, what are options telling us?

OI for BTC taken from laevitas.ch

OI for ETH taken from laevitas.ch

If you haven’t checked out the dashboards on Laevitas I definitely recommend them. It’s tough to get directional info from options activity but you can’t completely discount that Deribit traders have been heavy on BTC calls @ $70,000 and ETH calls @ $5,500. Key areas to watch, for sure.

Sunday, let alone being a weekend, is rarely an important day for cryptos in general. Given the number of false starts that riddled the month it’s easy to dismiss this price action as just another false pump. However, along with being a psychological milestone for crypto, October 31st closing daily is vitally important to maintaining S2F trend and supporting the overall cycle narrative. October was always supposed to be BTC “Uptober” and the prophecy was fulfilled on the 20th after BTC broke ATH, with ETH breaking its ATH only 9 days after. Bear FUD reached also reached ATH calling for cycle top with ZH making an all-too-early call on ETH breakdown (which I couldn’t help but call out myself):

Grade-A Twitter shit-talk

Dan’s on-chain analysis has strong support for BTC continuing its big move through November. Decent probability of a supply-shock related pump and most of the market being long at this point tells you everyone is thinking the same thing. Whales have done a good job of crushing lev longs throughout the month so funding has been kept low along with OI. One of the bigger questions remaining to be answered over the next few days is the state of alts in the expected BTC run-up. Alt season index hit a high of 65 on the 26th, and with SOL seeming to lead each of these alt pumps we could be at the starting gates for a very frothy November. I couldn’t help put on a lev long on SOLPERPs a couple weeks ago (and have been suffering through some whipsaws on funding throughout) and personally can’t wait for these to be deep in the black over the next two weeks. From where came this sudden fervor in SOL, you ask?

This is looking eerily similar to the ETH/BTC ratio breakout that helped ETH outperform BTC in 2017 on a % ROI basis. Should this pattern play out again we could see SOL not only outperform BTC but also ETH, now a mature asset in its own right, which has seen its own volatility decline with increases to futures OI over the past year. Even if it fails to live up to the hype (we are still bullish on ETH 2.0 merge in the long-run) the important thing is traders are pricing it like ’17 ETH this cycle, helped every now and then by the occasional SBF/FTX smash-buy, making this one of the best EV trades of the year. We’re keeping an eye on this one.

Almost everyone did a 10-year anniversary of Satoshi Nakamoto’s publication of “Bitcoin: A Peer-to-Peer Electronic Cash System” on October 31st, 2008. TruBlock decided to do something a bit different. Instead, we will be commemorating Jamie Dimon’s famous declarationon September 12, 2017 that Bitcoin is a ‘fraud that will eventually blow up’ with an article devoted to covering JP Morgan, and Wall Street’s, friends-on, friends-off relationship with crypto.

It is unlikely that Jamie Dimon ever intended to become the poster boy of crypto criticism. With the departure of Lloyd Blankfein from Goldman’s helm in September 2018 there are few other active Wall Street titans with the interview face time (and rumoured political aspirations) as the 18-year head of JP Morgan Chase. Interestingly though, the two have persistently held differing views on crypto with Blankfein making a point of leaving the door open’ when it comes to answering crypto-related questions in interviews. Bloomberg posted an article on the dichotomy of both men who quite literally grew up in the same city, began as CEOs of the two largest banks on Wall Street within six months of each other, and led their respective companies through the worst financial crisis in decades. The article goes further to describe Dimon as the ‘sometimes ill-tempered alpha male from Queens’, a character trait that could explain his recent snap when asked about Bitcoin at the Axios conference on Wednesday. Bloomberg has long been tracking Bitcoin bulls and bears, and while there is a long list of prominent economists and bankers opposed to Bitcoin much of the media’s fascination with Dimon is his public reactions when asked about it. So what is with negative reaction? And why does Goldman appear bullish on the upstart tech? Perhaps it has more to do with how the two banks operate-

Figure 1: JP Morgan Annual Filing 2017, Total Revenue by Segment

To be clear, while the two banks provide competing products and services they operate in different market segments: Goldman’s services focus is in securities and investment brokerage while JP services consumer, corporate and commercial banking, more traditional bank lending. Total revenues from what JP terms Consumer & Community Banking, comprising the traditional consumer loan, card, and mortgage provision business, made up 45% of total firm revenue in 2017. While the investment banking business made up 33% of total revenue less than half of that was from underwriting (principal transactions); the rest were fees. Asset Management makes up only 12% of total revenue and is mainly commission driven through its mutual funds and wealth advisory services. With that being said, as of 2017 it is the largest asset manager in the world with US$2.789 trillion in assets under management and US$30 trillion in assets under custody. Depository and custodial services are a core revenue stream for the bank as it is able to charge commissions on clients, as they say, ‘coming and going’. JP Morgan fared better than most banks post-2008 crisis because these traditional banking services helped steer it away from MBS exposure. The bank was also a prime beneficiary of the Fed’s credit expansion policies post-2008 as they provided a strong uplift to deposits and lending.

Figure 2: Goldman Annual Filing 2017, Operating Results by Segment

Goldman is undoubtedly more securities-centric with its Investment & Lending and Investment Management segments comprising 40% of total revenues. While a good portion of this consists of fees the majority of revenue in fact comes from commissions through underwriting and origination. Compared to JP a larger percentage of Goldman’s IB revenue came from underwriting vs fees. To elaborate further, a significant chunk of total firm revenue was derived from its Market Making business which totaled $7.7B or 26% of all non-interest revenues. While it is difficult to cleanly segregate market making from divisional revenues it is clearly a larger portion of the overall pie, reflecting the reliance of Goldman’s core business on services related to securities origination, private placements, brokerage, and liquidity provision. Goldman is also more positioned toward servicing private and institutional clients, avoiding the consumer and retail markets almost entirely. This forces Goldman to be more creative with its core business and adopt a more risk-taking approach relative to its peers. Further to this point, Goldman for decades has established itself as the prominent trading desk on Wall Street boasting some of the highest trading revenue among the big banks with its commodities desk raking in $3.4B in 2009, capitalizing on the wider commodities boom of the late 2000’s.

Goldman’s revenues from its fixed income business have been sliding since the crisis in Greece, declining on average 20% normalized year-over-year. Its fixed income trading division posted quarter results ending 2017 of $1B, nearly what it was making every two weeks throughout 2009. With declining revenue from its trading divisions, and credit markets inevitably shrinking in the immediate future as a result of the wider deleveraging, Goldman will need to find new revenues streams to make up for the gap in its earnings. Enter crypto.

The concept of Initial Coin Offerings is salivating to a firm that generates almost half of its revenue from the creation and trading of securities. Not only does the ICO industry represent an untapped market for legal and financial advisory the underwriting possibilities for banks like Goldman are limitless. While many ICOs have been carried out without help from financial institutions, as was the original idea, its unlikely that this will continue without regulator oversight. The SEC posted a bulletin in August 2017 warning investors of ‘pump-and-dump’ ICOs, with Bloomberg BNA reporting the regulator is now currently investigating a number of ICOs it suspects are in violation of US securities law. Greater regulation will force new startups to consider retaining the services of firms like Goldman to help underwrite their ICOs. The inevitable next step is for Goldman to provide market maker and principal placement services which augment their existing service lines. Rumors persist of Goldman launching a crypto trading desk to profit off the historic volatility and provide Bitcoin derivative products to its clients. This would be a natural extension of their existing OTC derivatives business. After the Volcker rule was reinstated as part of Dodd-Frank in 2010 Wall Street banks have been prohibited from operating proprietary trading desks, although with Volcker 2.0 on the table banks may revisit a more exciting era of risk-taking.

Does JP Morgan see the same opportunities in this emerging asset class? Maybe. Some are hypothesizing that Blankfein and Dimon’s opposing views on Bitcoin are a media stunt designed to spur interest. While this is purely speculation there is some support for this theory in the sense that, in the case of Dimon, JP Morgan’s investment in Quorum and foray into crypto-solutions does not align with his publicly stated views. The bank hopes to use Quorum, an enterprise version of Ethereum, to tokenize gold bars as part of its global commodities trading and custody business. Such a move would be a major step forward in terms of moving commodities trading that is already taking place onto a blockchain platform. JP Morgan is also an investor in Digital Asset, a company which is building a blockchain clearing house for equities traded on the Australian Stock Exchange. Surprise surprise, Digital Asset is headed by JP Morgan alumnus Blythe Masters. With all of these investment being Ethereum based perhaps Dimon is being specific about his hatred for only Bitcoin. As well, these are all private ledger platforms and Dimon has been public about his outright rejection of public blockchains to manage proprietary client data.

What is clear is that Bitcoin itself was created, and currently exists, to disrupt the traditional financial intermediary business. The concept of someone holding your money and moving it from place to place, for a fee, is under attack. JP Morgan has every reason to shut down a technology that eats into its retail deposit and client card revenues. The question is -will it go down without a fight?

Despite the considerable progress smart contracts have made in a short period of time there has been comparatively little real discussion of their specific advantages. What is equally disappointing is how blockchain, crypto, and smart contracts all appear to be brought up in different contexts and are now confusing people. There was an interesting Verge article in March that made mention of this and how courts are starting to become confused themselves.

The Chamber of Digital Commerce published a White Paper in September that gave a great overview of smart contracts, and their operation within current legal frameworks. Interestingly, they drew a comparison of the requirements for a contract under US and Spanish law. In the US, and the majority of common law systems, a contract largely requires a “meeting of the minds” whereby a specific list of criterion must be satisfied: offer, acceptance, capacity, consideration, legality. Spanish civil law requires a similar agreement or mutual commitment, but instead centre around the concepts of consent, object of the obligation, and cause of the obligation. While smart contracts meet all of the above criterion, thereby acting as a potential bridge between wholly different legal systems, the primary benefit smart contracts provide is the ability to automate the origination, execution, and disputes to the contract and its terms. The packaging of contractual terms goes as far back 1996 by cryptographer Nick Szabo in his paper ‘Smart Contracts: Building Blocks for Digital Market’:

“The basic idea of smart contracts is that many kinds of contractual clauses (such as liens, bonding, delineation of property rights, etc.) can be embedded in the hardware and software we deal with, in such a way as to make breach of contract expensive (if desired, sometimes prohibitively so) for the breacher.”

The fundamental utility of smart contracts is that while they contain the basic mechanisms that underpin legal contracts across the various jurisdictions, the inherent beauty is that code itself is the law governing the contract. The judge, the lawyers for both parties, the executor, the witness -all are embedded in the code and at all times executing on what was originally agreed upon by the parties.

Levi and Lipton, attorneys at Skadden outlined inherent legal limitations to smart contracts in a post on the Harvard Law School Forum. They begin with the most widely used example of smart contracts regulating escrows and trusts, or for that matter any transaction which requires “(1) ensuring the payment of funds upon certain triggering events and (2) imposing financial penalties if certain objective conditions are not satisfied“. Citing Szabo’s famous vending machine example, the authors describe how the majority of human involvement in execution and enforcement of similar transactions can be removed, ultimately reducing cost. Chain-of-custody administration is another low-hanging-fruit example of how blockchains are reducing cost, as noticed by the shipping industry. The reduction of cost will ultimately be the impetus for widescale smart contract implementation. However, along with the benefits of automation come inherent limitations, and risks. To name a few:

Difficulties for non-technical parties to negotiate, draft and adjudicate smart contracts

Reliance on off-chain resources to execute smart contracts, eg. third party websites for reference information as a condition prerequisite

The dangers of automation, or limitations for humans to amend/follow the contracts once they begin executing on their own

Objectivity and the difficulties in finding applications outside of if/then conditionality contracts

Interestingly enough, one of the more frequently mentioned concerns with smart contracts is the scenario in which the ‘robots run amok’. This was a widely held fear of high frequency trading (HFT) that has since been thrown out. While algos have contributed to increased volatility, as witnessed by the most recent market correction in February, some are arguing they are simply acting to deepen sell-offs or exaggerate run-ups that are already occurring. Kutsayama and Lewis’ book Flash Boys put HFT at the centre of the debate when they published “Flash Boys” in 2014. Kutsayama to this date does not rule out the benefits HFT has brought to the the market such as price discovery and added liquidity. To put it simply, while coding algorithms remains within the domain of coders this has not slowed down their integration into global exchanges.

In relation to the law, misfiring transactions are currently handled through litigation and it would not be difficult to see the same here, involving technical experts and judges dissecting misfired smart contracts. In most cases, smart contracts are put through a test environment before launch and standards will inevitably emerge over time. In fact, regulators in the United States and Canada have established FinTech sandboxes to allowing companies to test algorithms in the past, and now more recently, registration of ICOs prior to their launch. Angela Walch published an excellent paper in March 2017 stressing how regulator’s education of the technology was essential to its proper governance.

While there are some challenges ahead for widespread smart contract adoption their future impact cannot be ignored. Algorithmic trading is an example where technical and regulatory challenges were overcome by more powerful economic incentives. Regulators are more eager than ever to support financial innovation in the crypto-space. The legal framework, despite its reliance on written case law and human actors, was designed with mechanisms that can be automated via smart contracts. Levi and Lipton both reference the Uniform Commercial Code that states ‘agreements do not always need to be in writing to be held enforceable.’ Individual States in the US have gone further to enact crypto-friendly legislation, albeit clumsily.

It appears the line between smart contracts and the law is becoming more seamless by the day.

On August 20th we briefly looked at the all-time-high in BTC short positions is developing on Bitfinex and how it can potentially be used to predict inflection points in the price. What is beginning to look more interesting is the fact that the net long/short positions on Bitfinex BTC and net long/short Managed Money positions on the COMEX are both currently at record lows. While it is too early to draw a direct relationship between the two it is important to consider that BTC has been likened to gold on more than one occasion, and that any emerging correlation would have huge implications for BTC as an emerging asset class.

Figure 1: TruBlock Capital Research, COMEX, CFTC data

Gold has been steadily increasing since its low at the start of 2017 as investors have been relatively nervous about equities reaching all time highs. The CFTC first reported net managed money positions went negative on June 26th with gold prices at $1256.60/oz. Since the start of 2018, particularly after the market was able to shrug off the equities crash in February, hedge funds have been shorting gold believing that a correction in equities had occurred and risk was back on the table. This strategy worked in the short term as the downward pressure on price encouraged further selling. The danger lies when the price no longer responds to increasing shorts and the market starts to move the other way, forcing these shorts to cover, sending price surging upwards. These net long/short positions hit an all time low in October 9th with a gold price $1,193.10/oz. Hedge funds have been historically famous for shorting gold at the bottom and it appears the same reversal is starting to play out all over again. The last time this happened in early 2016 gold prices made a subsequent 30% increase over the course of seven months.

Figure 2: TruBlock Capital Research, Bitfinex

Looking back at the net longs/shorts on Bitfinex, as was first mentioned in August, the net neutral periods loosely marked inflection points in price prior to a run up. The clearest examples were at the start of April when the price found a floor at a low of $6,450. As longs gained more confidence, and the net position went even higher, the price climbed back down until hitting the same resistance, at which point the net position went neutral again marking the start of the second rally in June-July. What is different this time is how the net position has been persistently negative over the last three months with little response from price. With record lows in the net position present in both markets we need to ask whether a similar short squeeze is starting to develop in BTC.

Fundstrat, Bloomberg, Market Data

BTC has historically had a low correlation with other asset classes, including gold. Funsdtrat’s Alex Kern and Ken Xuan published results of their study on BTC correlations in August, the results of which can be viewed in Figure 3 above. The National Bureau of Economic Research have confirmed these findings in a working paper published later that month titled “Risks and Returns of Cryptocurrency”. For daily tracking, Sifr Data has a great site which tracks the 90, 180 and 356-day correlations of each coin with the S&P and gold. It will be interesting to monitor this relationship over the next few weeks as the general slowdown in markets takes hold increasing investors’ flight to safety.

The continued selloff in US government bonds, and resulting rise in the 10-year yield, is making the bond market white-elephant-in-the-room more difficult to ignore. While this more recent shock was precipitated in late September after the Fed raised rates to 2.25 percent, marking the end of the Fed’s ‘Accommodative Policy’, the underlying causes have been at play for some time.

Figure 1: TruBlock Capital Research, St Louis Fed Data

Figure 2: TruBlock Capital Research, US Treasury Data

With US national debt soaring to new heights each year purchasers of US treasuries (namely China) have become concerned with the continued ability for the country to pay it down. Data from the St Louis Fed shows the Debt-to-GDP ratio increasing substantially right after the ‘08 financial crisis as the Fed began its policy of quantitative easing. Between 2008 and 2015 the Fed’s balance sheet ballooned from $900B to $4.5T in purchases of government bonds and mortgage backed securities through the troubled asset relief program (TARP), allowing the financial sector to unload most of the toxic assets it was holding on commercial bank balance sheets. While the Fed was able to avert the immediate crisis the country’s Debt-to-GDP broke the 100% mark in 2013, a milestone for a country with $16.8T owed not only to foreign countries but a large amount to itself. Ignoring the fact that almost any other country would face an immediate currency devaluation if their central bank began purchasing it’s own country’s debt to tautologically save it’s own economy, the concern to foreign buyers of US debt is that now there is a concern the US will eventually no longer be able to meet it’s debt interest payments. Since 1988 the US government interest expense on debt outstanding, or the amount paid to service the US government debt, has doubled to $500B. If this trend continues at the current rate debt maintenance will overshadow medicare and military spending within a decade. What is the most troubling is that this has all been happening during a prolonged period of falling bond yields, until now:

Figure 3: TruBlock Capital Research, St Louis Fed Data

This is extremely worrisome for investors for a number of reasons. Firstly, as the selloff in bonds indicates a lack of appetite for 10-year US treasuries (and other forms of long term debt) we have to be concerned that the selloff in bonds is pushing yields higher. Part of the move is the market simply staying ahead of future intended rate hikes. However, if the selloff in bonds continues a larger correction could be taking place, and as the chart above indicates yields have been breaking out of a longer term band since the start of 2018. Higher yields are particularly bad for equity markets as they are usually a leading indicator for higher borrowing costs for corporates and households.

Figure 4: TruBlock Capital Research

Figure 5: TruBlock Capital Research

The impact on corporate earnings from higher debt costs is clear. The drop in the Russell 2000 was more pronounced, and came earlier, than the S&P 500 as it comprises a basket of riskier companies more sensitive to interest rate changes. Both the most recent shock and the one in February were preceded by a steep jump in the 10-year yield. It will be interesting to see what the prolonged impacts of higher yields have on equity markets as households begin to feel the effects from rising mortgage rates lowering disposable income (and consequently consumer spending). It will also be interesting to see if the sudden drop in equities is a short-term correction to an overextended stock market, or if this is really the start of a larger correction across all asset classes. With that being said we need to turn our attention to yield curves and their ability to predict US recessions.

Figure 6: TruBlock Capital Research, US Treasury Data

Figure 6 charts three treasury yields at varying durations to illustrate a ‘flattening’ of the yield curve for government debt over time. Each of the periods where the lines converge, indicating the market is trading all three bonds at the same value, has occurred in the run-up to a major US recession. To further elaborate, the curve allows for a quick comparison of shorter term bonds versus longer term bonds. A ‘normal’ yield curve is depicted by a rising yield as the bond maturity increase and is typically is the sign of a healthy expanding economy. However, as the government starts to increase short term interest rates, and investors begin to flock to less risky assets such as short term treasuries, the yield curve begins to flatten. The concern is when the market starts to value short term bonds so that the implied yield is higher than longer term bond yields creating an ‘inverted’ yield curve (eg. short term treasuries momentarily went negative during the 2008 crisis). An inverted yield curve implies that the market is demanding short term bonds over longer term bonds, and this has historically been the precursor to a market contraction (it is a flight to safety).

Figure 7: TruBlock Capital Research, US Treasury Data

Figure 7 charts the difference between the 10-year and 2-year yields to more clearly show these yield convergences over time. Red shaded areas illustrate official US recessions. Important to note that once the market does decide to go negative it has happened fairly quickly. While dollar appreciation and rise in demand for short term US treasuries continues to occur during market selloffs the appetite for long term US debt is of grave concern. Although the creeping 10-year yield is a problem for corporates and households it is primarily a problem for the US treasury. As yields rise so do the interest payments owed by the US government. Not only does the US owe a ballooning national debt but the cost to service that debt is on the cusp of a dramatic increase.

As the economy begins to contract, and the Fed continues to raise rates to combat inflationary pressure, and demand for shorter term bonds continues as further flights to safety ensue, the long term effect is that holders of US treasuries may eventually lose their appetite for future issuances. What everyone should be worried about, and what nobody wants, is a self-fulfilling-prophecy or uncontrolled and violent deleveraging to play out. Quantitative easing and asset purchases by the Fed were able to avert a disaster in 2008, but we are beginning to see that this may have come at a significant cost.